The latest Paycheck Protection Program legislation will significantly change both Originations and Forgiveness.

Numerated is here to help. We’ve put together a brief roundup of the questions most frequently asked by our customers and curious bankers alike.

As with our PPP FAQ for Banks and Credit Unions, we’ll do our best to keep this resource updated as new information becomes available.

In the meantime, we encourage our readers to keep an eye on official sources of information.

A Note on the Jan. 6 IFRs

On Jan. 6 the Treasury Department released two Interim Final Rules, the first of many expected as the program nears reopening. The IFRs outline amendments to the original Paycheck Protection Program and, for the first time, outline requirements for Second Draw loans.

The much anticipated guidance totals 124 pages across both IFRs and introduces significant complexity to PPP Originations, specifically around Second Draw loans. Through it’s IFRs, the Small Business Administration and Treasury have established different regulations by industry, have provided different calculation methods borrowers can use to determine their loan amounts, and will require multiple types of documentation from borrowers throughout the process. This will likely make applying for a Second Draw loan feel more like navigating the tax code for borrowers.

As part of our commitment to simplify this process for borrowers and lenders, we’ll be providing a breakdown and analysis of this guidance on our PPP Prep and Launch Week Q&A Sessions each day at 3pm EST. Register for today’s session here.

Frequently Asked Questions by Banks and Credit Unions on the New PPP Legislation

What is in the new legislation?

This new bill provides $284B to the Small Business Administration to reopen PPP Originations and provide second draw loans for eligible businesses.

The new legislation will help simplify forgiveness for new PPP loans totaling $150,000 or less. The SBA will release a new, simplified form, for this, though timing for this is still TBD.

The bill also provides clarification on borrower eligibility and usage of funds. Eligible businesses that have already depleted their PPP loans will now be able and likely to apply for a second one. The demand for these funds should not be underestimated.

What is the timing to implement regulations for the bill?

- The SBA has 10 days from the enactment of the bill to establish regulations that carry out the bill.

- The SBA must publish a new one-page form within 24 days of enactment.

- The start of PPP applications of any kind is TBD.

What are the new allowable and forgivable uses for PPP loans?

- Operation expenditures related to payment for any software, cloud computing, human resources, and accounting needs are now covered.

- Property damage costs: Property damage caused by public disturbances that occurred during 2020 and are not covered by insurance are now an allowable use of PPP funds.

- Supplier costs: Payments to suppliers for essential goods made via a contract or purchase order enacted prior to taking out a loan are now covered under PPP.

- Worker protection expenditures: New coverage includes personal protective equipment and other investments to help a loan recipient comply with federal and local health and safety guidelines between March 1, 2020, and the end of the national emergency declaration.

- Other costs for adapting to COVID-19

Changes to Originations

Originations now includes 3 variations:

- New first draw: Businesses that qualified but never received a loan

- New second draw: Business that received and used a first draw, and want a second draw

- Expanded first draw: Interim Final Rule (IFR) entitled companies may request more first draw money, as an expansion rather than a second draw

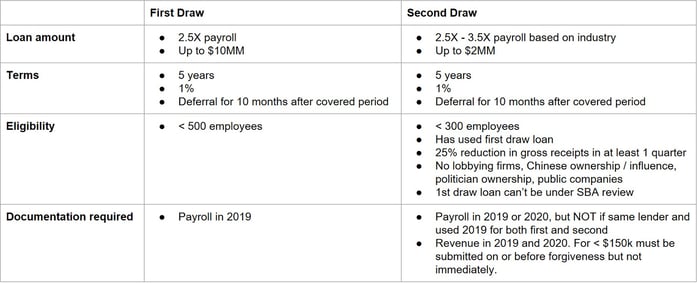

What are the key differences between first and second draw loans?

The key differences between first and second draw loans can be seen in the table below:

What forms will be used for first and second draw loans?

- Borrowers taking out a first draw loan will used the revised Form 2483. A corresponding lender form can be found here.

- Borrowers taking out a second draw loan will use the new Form 2483-SD. A corresponding lender form can be found here.

What limitations are there to second draw loans?

Second draw loans are limited to businesses with:

- 300 or fewer employees

- 2.5X monthly payroll (same as first draw), up to $2MM (down from $10MM)

- There is an increased loan amount available to businesses in Accommodations & Food Services (NAICS 72) of 3.5X monthly payroll

- Show a 25% decrease in quarter-over-quarter gross receipts

- Loans < $150K only require borrower attestation for annual sales decrease

What are the major differences a business must meet to qualify for a second draw loan?

- Businesses must have used or will use all funds from a first draw loan.

- A business or organization that was not in operation on February 15, 2020 is not eligible for a first draw PPP loan and a second draw PPP loan.

- Eligible entities that receive a grant under the Shuttered Venue Operator Grants are prohibited from obtaining a PPP loan

- New restrictions on China-related entities

- No entities created or organized in China

- No entities in which China owns more than 20%

- No entities with a board member living in China

How long are funds available?

PPP funding is available until March 31, 2021 or when the funds are depleted.What is the maximum dollar amount that a business can request?

The maximum eligible dollar loan is $2M.Did the Covered Period for Forgiveness change?

The covered period is any date between 8-24 weeks, not to extend beyond Sept. 30, 2021.When does the Forgiveness Covered Period end?

The coverage period has been extended from December 31, 2020 to September 30, 2021.What are the new lender reimbursement rates for processing?

- For loans up to $50K, lender fees are either 50% or $2,500, whichever is less.

- For loans between $50K-$350K, lender fees are 5%.

- For loans totaling more than $350K but less than $2M, lender fees are 3%.

- For loans of at least $2M, lender fees are 1 percent.

What supporting documentation must a business provide?

- For loans up to $150K, no supporting documentation is required for the application or Forgiveness. However, borrowers must retain the supporting documentation for four years.

- There are no changes for loans over $150K.

How will Numerated support changes to originations?

- Support concurrent applications across multiple product types with a single borrower portal: first draw, second draw, first Forgiveness, second Forgiveness

- Numerated will support all entity types and borrower types:

- Existing PPP borrowers

- Existing customers without PPP loans

- New customers (if desired)

- Simplify & streamline the process using data from earlier rounds of PPP, the bank and the SBA

Changes to Forgiveness

Will lenders be held harmless for any misrepresentation by borrowers?

Lenders will not be liable for borrower misrepresentations. In applications where there are no documents to review, all lenders are required to do is ensure an application is complete. This check can be performed by the Numerated system.Should the EIDL Advance no longer be deducted from forgiveness payments?

The Economic Injury Disaster Loan (EIDL) Advance should no longer be deducted from forgiveness payments and needs to be paid retroactively to borrowers. The SBA has 15 days from enactment of the bill to issue details on how this process will work.How will Numerated support Forgiveness changes?

- Numerated will completely automate forgiveness requests under $150k, with no work required from the lender.

- The new short form will be over 75% pre-filled.

- No supporting documentation is required

- There will be options to automate the lender review step and skip the lender cosign.

- Numerated will also develop support for transitioning in-flight requests, once form changes become clearer.