For years, banks and credit unions have been warned about the encroaching competition of nonbank lenders.

These are the fintechs like Square and Kabbage, and tech giants like Amazon, that lend directly to small businesses through their online platforms. While they tend to charge higher rates than their bank or credit union counterparts, the level of speed and convenience they provide customers has allowed them to grab larger and larger pieces of the commercial and industrial (C&I) lending pie.

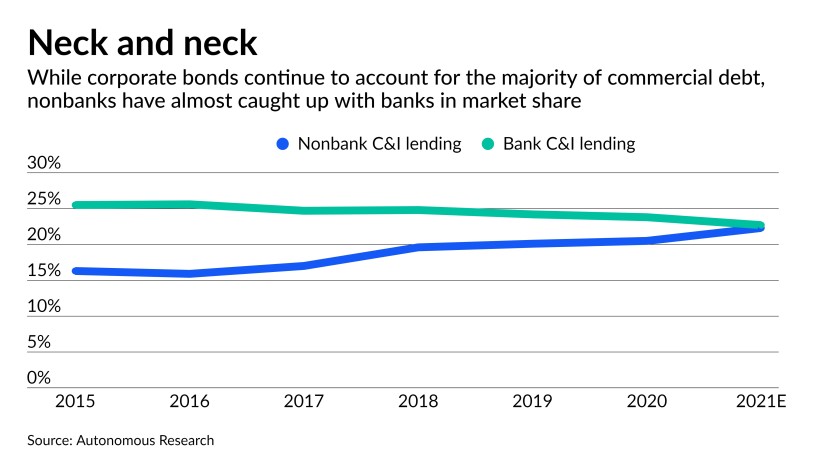

Even still, traditional financial institutions have historically held more debt in the small business lending segment. Until 2021, that is.

According to recent reporting in American Banker, new projections from Autonomous Research, “which analyzed data from the Federal Reserve’s most recent Flow of Funds report,” show that by the end of this year, nonbank lenders will hold roughly the same amount of C&I loans as banks and credit unions. By the end of Q4, the report details, traditional financial institutions will hold just 24 percent of all C&I loans while nonbanks will hold 23 percent. In 2015, traditional financial institutions accounted for 26 percent of all C&I loans, to nonbanks’ 16 percent.

This is a significant milestone for the evolution of the small business lending segment and could represent a competitive tipping point, where nonbank lenders become the go-to option for small businesses.

As far back as July, we began to see our first hints of this shift. Back then, we wrote about a report in International Banker that showed how customers’ expectations were changing to prefer digital-first experiences during the pandemic. We also looked at a report from Bain & Company that showed when customers couldn’t get a digital experience from their primary institution, they would find that experience elsewhere.

Now, projections from Autonomous Research seem to confirm these previous findings.

The key takeaway for banks and credit unions is that they can no longer ignore this growing segment of their competition.

If traditional financial institutions want to keep their current customers and continue to be competitive for new ones, they’ll need to take a hard look at nonbank lenders and the advantages they provide their customers.

Speed and convenience is key here. Today’s business owners are ultimately consumers as well. They’re looking for the same level of convenience in business banking as they get from making purchases on Amazon, or in finding a new show on Netflix.

If banks and credit unions can adopt technology that allows them to do so, they can level the playing field and once again compete on factors more favorable to them—like interest rates or customer service.

The Numerated Digital Lending platform is purpose built for business banking and can help banks and credit unions compete and win against their nonbank competitors.

The platform dramatically reduces work for financial institutions and their customers using data—providing the best customer experience available and saving bankers 3-4 hours on doc prep, per loan.

Today, more than 400,000 businesses and 1 million users have leveraged the platform to secure more than $50B in lending from the more than 140 institutions partnering with Numerated.

To learn more about the Numerated Digital Lending Platform and how it can help your institution take the work out of business banking, contact us today or register for one of our biweekly webinars, by saving your seat here.