A strategic initiative all financial institutions should implement is the review of every journey they ask their customers to take when interacting with the products and services they offer. Oftentimes, many opportunities for improvement will be found to increase competitiveness, customer loyalty, and internal efficiencies.

Let’s take the process from loan application to deposit account opening and funding as an example. Most lenders require their business customers to maintain a deposit account with their institution to receive funding for a loan. In order for lenders to win that entire business banking relationship, it’s important they evaluate what their current loan origination and deposit account opening process looks like to identify bottlenecks in the customer journey. Many times, lenders do not recognize the difficulty and complexities of their processes, until they sit down with their employees at the branch level.

It’s during these discussions when they find that applying for a loan and opening a deposit account is a very cumbersome paper-based process. Although these processes may seem to be functional at a high level, they’re not scalable, are prone to risk of creating a bad customer experience, and also put the institution behind the current customer expectations of an efficient digital process, limiting the lender’s ability to compete online.

In order to holistically understand the entire customer journey, lenders should look at each step of the process and identify areas where technology can improve it. This can be accomplished through creating a customer journey map.

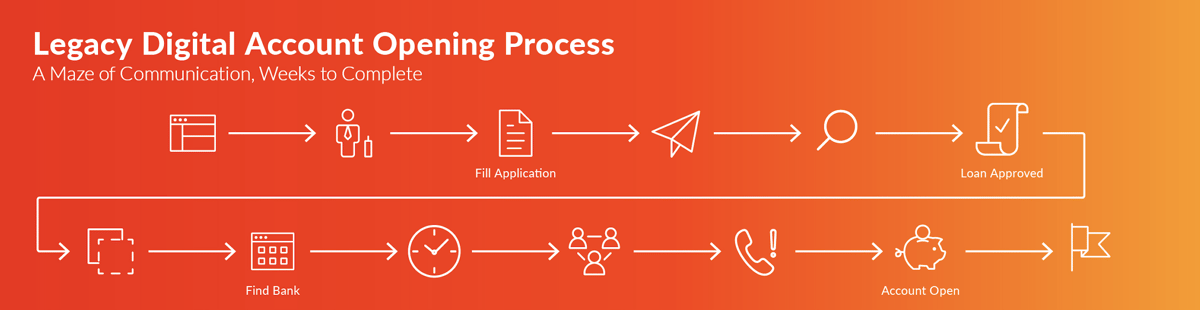

The Customer Journey Map for Legacy Loan Application and Deposit Account Opening

Customer journey mapping is a technique used by businesses in many different industries to better understand the step-by-step path their customers take to purchase a product, or in this case, receive funding for a loan.

To understand what a typical customer journey looks like for a business borrower seeking a loan from a legacy institution, we spoke with a bank that had yet to digitize their borrowing experience.

By operating on a disjointed process with many customer touch points, they identified at least 13 steps requiring action from the borrower to continue their borrowing experience. Research has proven that borrowers are very unlikely to remain loyal to their current institutions if they can find a better experience elsewhere. With online-only fintech competitors providing small business funding weeks faster than traditional financial institutions, efficiency and convenience must be priority above all else.

A main point of friction in the legacy process is the back and forth conversations between the lender and borrower to collect all of the necessary information for the loan application. Oftentimes, this process could lead to the delay of funding by weeks.

One of the most difficult parts of the process is opening a deposit account after a loan is approved. If a business customer does not have a deposit account, there is an additional amount of work that needs to be done on both the borrower and banker side.

This process typically requires lenders to schedule a time to visit the branch to meet with a banker and provide even more information to open an account, which in turn continues to delay funding.

For many small business owners, the requirement of visiting the branch alone is enough for them to choose an alternative option simply because they do not have the time within business hours to do so.

In the chart below, we outline the entire customer journey of applying for a loan and opening a deposit account for a legacy lender.

This process can be as long as 13 steps including the following:

- The borrower visits the bank’s website to find contact information and waits for a response.

- The borrower speaks with a business banker to find out what information is needed to complete an application.

- The lender sends loan application documents for the borrower to complete and return to the bank.

- The borrower fills out the forms and either emails them or delivers them in person to the lender.

- The loan officer reviews and has additional questions and may require more documents from the borrower.

- The loan officer approves the borrower for the loan, but they still need to open a deposit account.

- The lender notifies the customer that they’re approved and they need to open a deposit account as a condition of loan approval.

- The borrower needs to make an appointment to visit the branch to open a deposit account.

- The borrower visits the branch and provides the same information to open a deposit account that they already provided to the loan officer.

- The borrower spends up to 30 minutes filling out paperwork and providing documentation before the account is open OR the banker is chasing down the client to even go into the bank to open the account before the loan gets funded.

- If the lender can’t get in contact with the borrower, there is continued back and forth with the branch employee and lender to get information that’s needed.

- The lender needs to keep contacting the borrower to request that they visit the nearest branch to receive funding for their loan.

- Once an account is opened, the lender needs to be notify the business owner to let them know their account is open.

This process is inefficient and will lead to a poor experience for the borrower, leading to loss of potential customers. If lenders want to remain competitive, they need to focus on creating experiences that will attract and retain customers in an increasingly digital-first lending environment. The bank we spoke to realized if they implemented Numerated technology to digitize their customer journey, they could cut the number of touch points down by 77 percent.

Creating a Customer Journey that Delights Borrowers

As borrower expectations change, lending processes should change along with them. Legacy lending processes can easily be transformed using the right technology.

Numerated empowers financial institutions to dramatically reduce work within the loan origination process for their employees and customers. Borrowers can receive approval for a loan within minutes, completely eliminating the back and forth of legacy processes. This significantly increases the amount of time lenders can spend nurturing their customer relationships and winning new ones.

After the loan application is approved, the need for a deposit account still exists. It’s important that the digitization of this process doesn’t stop at the loan approval.

When borrowers apply for a business loan online, they expect the ability to complete the entire process in one setting. The urgent problem for many lenders is they don’t have the technology that they need to create a solution that is end-to-end. They might have a digital loan application, but still require customers to visit the branch to open a deposit account.

Numerated is the only digital LOS on the market today that solves this problem. Using Digital Account Opening for Businesses, lenders can provide small business customers with an end-to-end solution enabling them to apply for a loan, open a deposit account, and fund the account via an integration with Plaid in one fast and simple application.

By investing in modern technology, lenders will increase internal efficiencies by removing multiple touch points and increasing available time to spend on revenue generating tasks, and they will experience a drastic improvement in customer satisfaction immediately.

The chart below shows how the complex legacy customer journey can be simplified into three easy steps using Numerated.

.jpg?width=1200&name=DAOProcess_Infographic_04%20(1).jpg)

Numerated has partnered with over 140 financial institutions to transform the loan origination process for business borrowers. In the last five years, the platform has processed more than $50 billion in lending to over 400,000 small businesses.

Learn more about how you can start transforming your business banking segment with Numerated by contacting us today.