Banks have another rapidly growing category of competitors to ward off in business lending: commerce technology companies, such as Square, PayPal, Shopify and Amazon. These companies are attacking banks’ long-held stronghold in business lending from the side, by building off of their technology foundations and relationships with businesses in commerce.

One thing is very clear: these technology companies are not being passive in their strategy and tactics to grow quickly and steal business market share from banks:

- All are offering a real-time lending experience;

- Most are using a business’ transactional and cash flow data to offer pre-approvals;

- Some are offering non-traditional financing in the form of merchant cash advances;

- Many are being creative in automating the paying down of debt;

- And all are using targeted direct marketing that pits fast-funding and convenience against the traditional bank lending experience.

The case of Square, PayPal, Shopify and Amazon

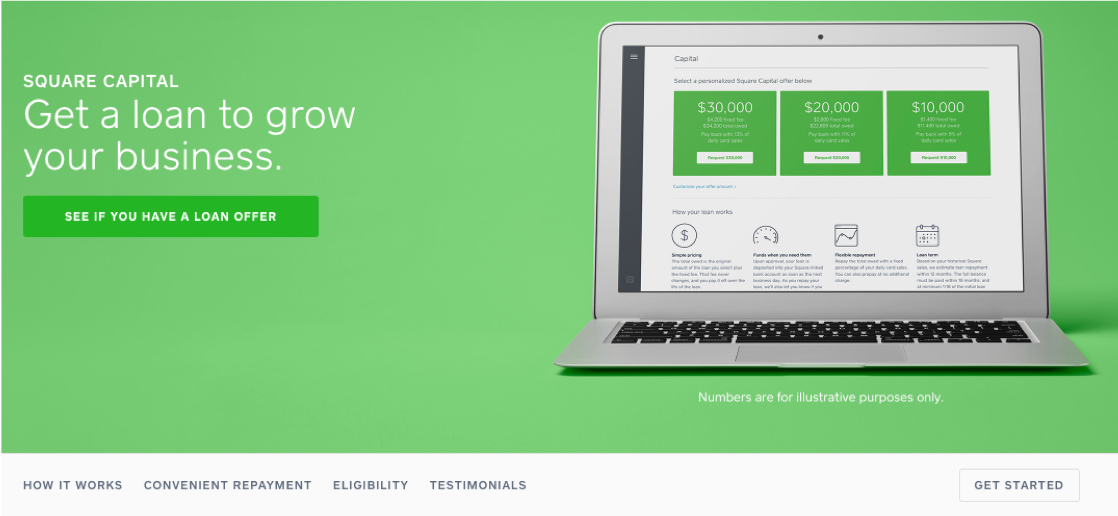

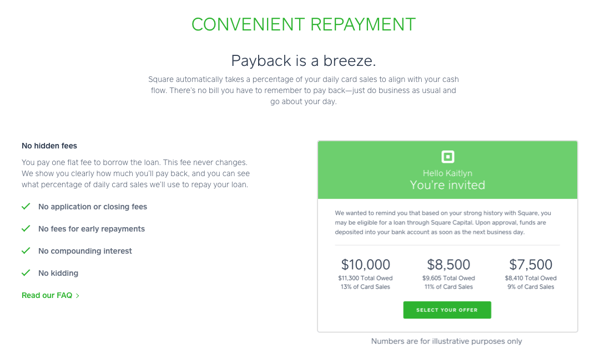

Square, through its Square Capital arm, has offered more than $2.8 billion in funds to over 180,000 business owners. Financing has ranged from $500 to $100,000 in the form of both traditional loans and merchant cash advances. The experience for business owners is 100% digital and fully automated.

[ Image Source: Square Capital ]

[ Image Source: Square Capital ]

Square is identifying and pushing targeted direct marketing of automated pre-approvals and next-day funding to businesses through the Square portal. And they are offering businesses the opportunity to automate paying down the debt by pulling directly from future sales transactions. The experience for the business owners is automated from end-to-end, literally at their fingertips at the click-of-a-button, and without any complexity.

PayPal is another example. They continue to press on the gas in business lending, offering a digital loan experience from $5,000 to $500,000, and more recently setting the stage in the merchant cash advance category with a $2.2 billion acquisition of a European payments startup.

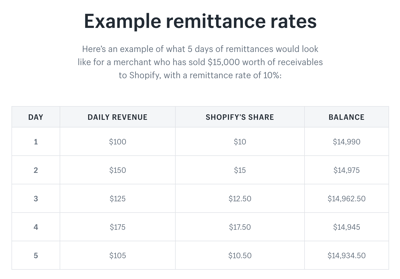

In ecommerce, Shopify is leveraging its trusted relationship with over 600,000 businesses as an ecommerce platform provider to now offer a business financing solution. It offers these businesses merchant cash advances at a range of remittance rates, allowing them to pay down the debt as a fixed percentage of their daily sales through the Shopify platform.

In ecommerce, Shopify is leveraging its trusted relationship with over 600,000 businesses as an ecommerce platform provider to now offer a business financing solution. It offers these businesses merchant cash advances at a range of remittance rates, allowing them to pay down the debt as a fixed percentage of their daily sales through the Shopify platform.

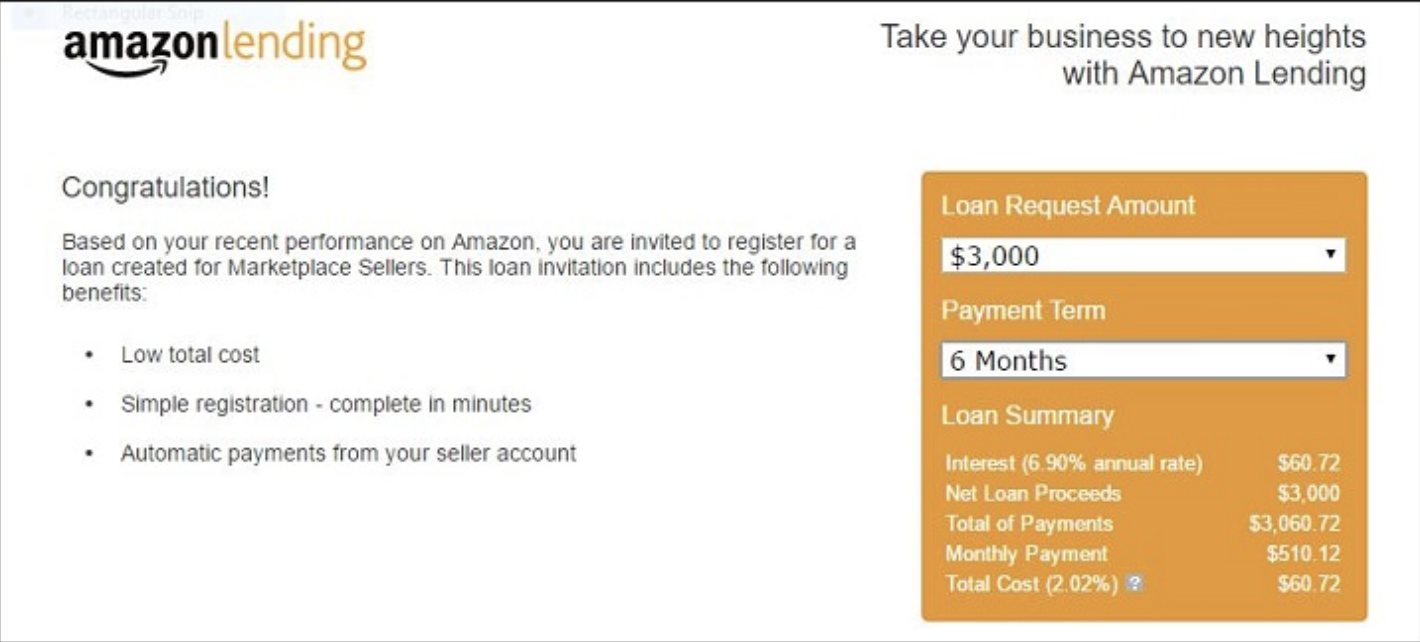

Drawing more attention, though, is tech giant Amazon, who’s invite-only and somewhat secretive Amazon Lending program has reportedly offered merchants loans from $1,000 to $750,000 for years. To say the company is moving fast to corner this market is an understatement. A year ago Amazon reported it had issued more than $1 billion in loans during the trailing year - up from a combined $1.5 billion in loans in the four years prior. Adding the the momentum are reports earlier this year of partnering with Bank of America for greater access to capital for the small business segment.

[ Image source: SecondHalfDreams ]

All of these payment and commerce technology companies are touting the convenience and speed of their business financing products vs. the traditional bank lending experience, and all are touting strong testimonials from business owners that pit their experience with these non-bank lenders against their expectations at traditional banks.

The good and bad news for banks

These moves follow nearly a decade of activity in the business lending space by alternative lenders offering businesses the ability to quickly and conveniently secure loans digitally online. However, the quantification of this competitive threat in more recent years has set alarm bells sounding in the C-suite of banks of all sizes across the U.S., with reports on non-bank digital lenders projecting a doubling of annual digital loan originations by 2021.

The good news: Banks can easily ward off the competition in business lending with their own real-time lending experience, by leveraging their trusted community relationships, and with more competitive rates:

- Banks can offer an equally convenient and fast digital lending experience;

- Banks have higher quality data to automate pre-approvals;

- Banks can be more intelligent at dictating the level of underwriting required for various sizes of loans and categories of applicants.

For example, Numerated’s platform offers banks more than just an automated credit decisioning engine and convenient real-time lending experience for businesses. It also ensures intelligent routing of loan applications in accordance with a bank’s credit policy and in support of both small and large loans. And for in-branch, over-the-phone, and on-site selling efforts, it arms retail and commercial bankers for omni-channel success with automated pre-approval data and targeted digital marketing to quickly close funding.

The bad news: Banks can no longer afford to wait to address the competitive threat; soon it will be too late. National financial institutions, alternative lenders and increasingly these payment and commerce technology companies are pushing an aggressive strategy to corner the business lending market, dictate the playing field, and win mindshare among businesses seeking financing.