.jpg?width=2501&name=Image%20from%20iOS%20(22).jpg)

Editor's Note: The following is an excerpt from our Playbook by Bankers for Bankers: Profitably Growing Your Small Business Lending. Get the full ebook, here.

Over recent years, high demand for CRE loans led many financial institutions to expand their portfolios. When COVID-19 hit, pushing many businesses out of their office spaces, it was a reminder of the need to find growth opportunities in new markets.

Many are finding that growth in the small business lending segment.

Unlike CRE, small business lending tends to be in the form of term loans and lines of credit, making them a more attractive option in our current low-rate environment than, say, a 20-year fixed rate.

Lending to small businesses also provides a number of fee opportunities and chances to expand your institution's share of wallet. For example, banks and credit unions use C&I loans to build relationships with businesses in their communities, providing them a natural opening to offer checking accounts, treasury services, asset-based lending, and other products that make these relationships stickier and more profitable.

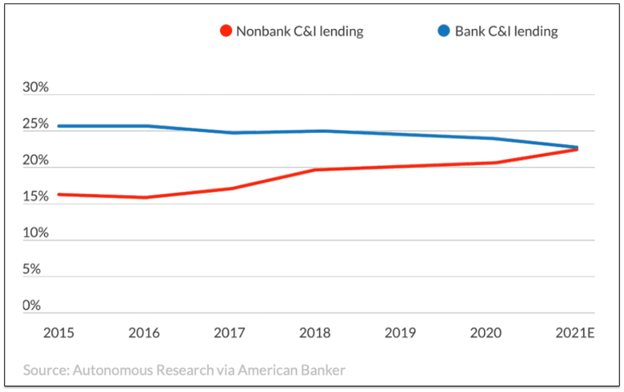

There’s currently high demand for these small business loans, too.

According to the July 2021 Senior Loan Officer Opinion Survey on Bank Lending Practices, from the Federal Reserve, banks and credit unions are seeing stronger demand for small business loans as well as more-aggressive competition from other banks and nonbank lenders in the segment. The same report notes slower demand for nonfarm, nonresidential real estate.

Some could argue there’s never been a better time to diversify into small business lending. And yet, many financial institutions struggle to do so profitably. This primarily stems from a lack of experience and tools, as few banks or credit unions specialize in small business lending and commercial loan origination systems are designed for larger and more complex credits.

As a result, many institutions encounter their first roadblock to success in the segment when they try to retrofit their existing CRE underwriting process—developed for high dollar, long-term loans—onto small business term loans and lines of credit.

While this copy and paste approach might work for the extreme high-end of C&I loans, banks and credit unions quickly learn that those whale-sized deals are hard to find, and even harder to win.

Rather than embarking on an endless search for the few small business loans that are sufficiently large enough to justify an inefficient origination process, leading institutions are deploying technology that takes advantage of data to dramatically reduce work for their teams and the clients they serve.

By leveraging tools like online applications, automated scoring, and digital doc prep, today’s leading institutions in the segment are able to support small business lending at scale and take advantage of where the bulk of the opportunity lies: term loans and lines of credit within the $20,000-$110,000 range, according to recent data from Fundera.

In the following sections, we’ll take a closer look at how banks and credit unions are profitably diversifying into small business lending with the help of today’s Loan Origination Systems.

This has been an excerpt from our Playbook by Bankers for Bankers: Profitably Growing Your Small Business Lending. Get the full ebook, here.