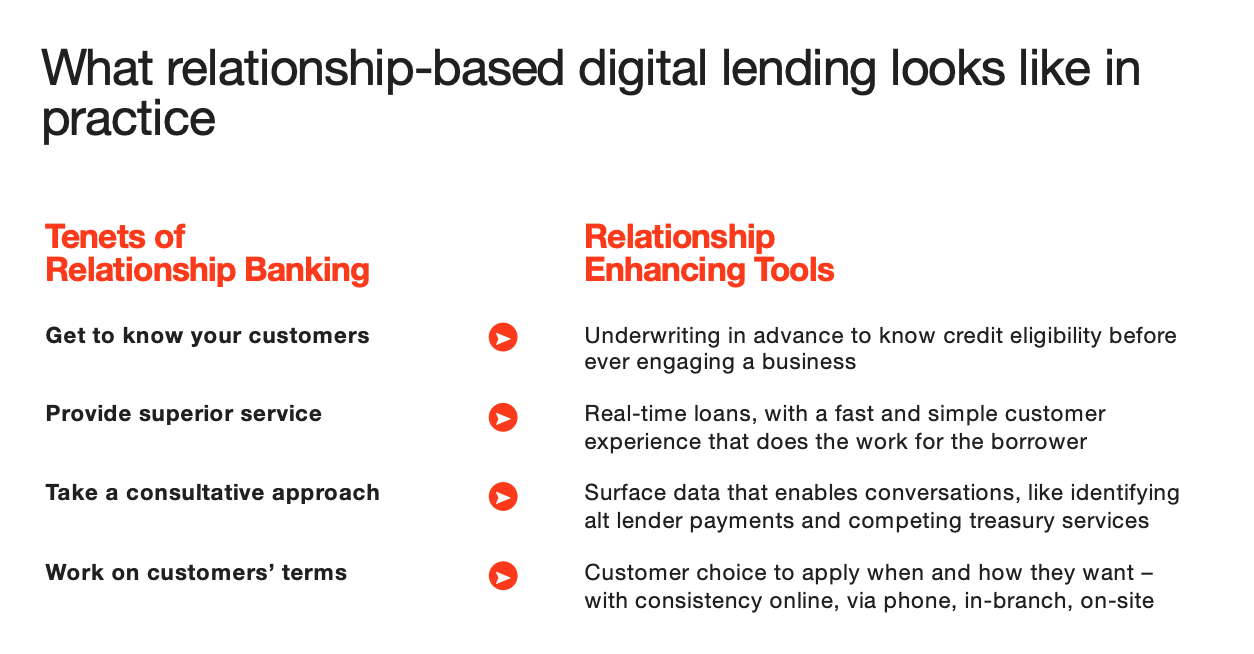

Relationship-based digital lending is the use of online technology in combination with traditional, relationship-banking tactics. Banks that implement relationship-based digital lending platforms and strategies are able to provide their customers with a digital-first experience, without totally replacing personal, banking relationships. Therefore, this type of strategy aims at leveraging big data and marketing and sales automation—as well as other digital tools—to help bankers identify, engage, close, and grow customer relationships.

Although capabilities will differ from vendor to vendor, relationship-based digital lending platforms help banks grow their business lending portfolios by reimagining how underwriting, sales, and the customer experience are executed.

In this post, we’ll provide a comprehensive look at relationship-based digital lending by touching on the following topics:

- How We Got To Relationship-based Digital Lending

- The Great Recession Setback

- Community And Regional Banks Have Fallen Behind Tech Trends

- Alt Lenders And Megabanks Are Using Their Technical Advantage To Target And Steal Community And Regional Bank Customers

- Community And Regional Banks Can Only Compete By Meeting Customer Expectations Through Relationship-based Digital Lending

- The Relationship Vs Digital Balancing Act

- Strategies For Banks In The Digital Era

To get an even more complete look at relationship-based digital lending, including case study data, watch our on-demand webinar with Founder and CEO Dan O'Malley.

How We Got To Relationship-Based Digital Lending

Before we get into the nitty gritty of how relationship-based digital lending works, why banks should favor it as opposed to digital-only lending, and why it’s a winning strategy for community and regional banks, it’s important to understand how we got here.

The Great Recession Setback

It’s been more than a decade since the Great Recession turned global markets upside down, but even today the effects of the worst economic crisis since the 1920s can be felt.

You’ll find no better example of this than in the US banking sector.

According to Karen Mills, former head of the Small Business Administration, prior to the financial crisis, the nation had about 14,000 banks. During her time at the SBA in the Obama administration, that number decreased to “about 8-9,000 banks.” Today, there are fewer than 5,000 banks across the United States.

Community and Regional Banks Have Fallen Behind Tech Trends

As we now know, the Great Recession created a survival-of-the-fittest environment for our financial institutions. Those still around today only survived by intensely focusing on their balance sheets from quarter to quarter, almost always at the expense of investments in growth and innovation.

But now that the Great Recession has given way to the longest economic expansion in history, banks are finding themselves in a precarious position. While Alt Lenders and megabanks poured billions into digital transformation, community and regional banks spent the last decade accumulating an unprecedented tech debt.

Alt Lenders and Megabanks Are Using Their Technical Advantage to Target and Steal Community and Regional Bank Customers

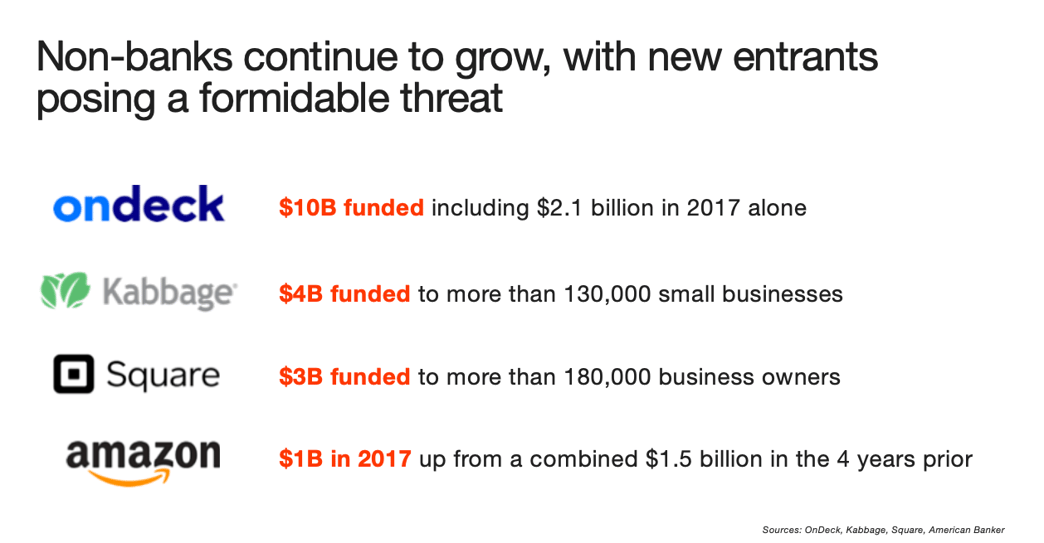

As these community and regional players began to see the light at the end of the tunnel and decided to switch from survival to growth mode, they found themselves playing on a field they did not recognize. They were no longer just competing against other community and regional banks. They were now competing with the likes of American Express, OnDeck, and Amazon—organizations with national reach, far more resources, and, at times, entirely different rules to play by.

Worse, Alt Lenders and megabanks aren’t just offering a more convenient and streamlined customer experience than banks have traditionally, they’re also using them to directly target community and regional banks’ best growth opportunity: business lending.

Community and Regional Banks Can Only Compete By Meeting Customer Expectations Through Relationship-Based Digital Lending

And, here’s where we come to the crux of the matter. Growth for community and regional banks hinges upon an institution’s ability to be competitive in business lending. The only way for these banks to win in this regard, is by beating the big guys at their own game.

By adopting digital-lending capabilities, and using them to bolster the relationships they already see as differentiators, community and regional banks can go beyond survival and begin thriving once again. What community and regional banks need is a relationship-based digital lending strategy.

The Relationship vs Digital Banking Balancing Act

Community and regional banks represent the backbone of the American banking industry and for more than 200 years they’ve provided unparalleled service by putting relationships front and center. But what happens when customer expectations change, and relationships are no longer the differentiator they once were?

We often refer to community and regional banks as “relationship banks” because of how central the customer experience and relationship is to their success. Should they really replace those relationships with technology? Or is there value in finding a happy medium?

As banks grapple with the challenges of the digital era and play catch up with Alt Lenders and megabanks, this is the fine line they need to walk. How do they “go digital” while still remaining relationship focused?

How Changes in Consumer Behavior Have Driven Demand for Real-Time Banking Solutions

Just as banks have always put the customer first, so too does a relationship-based digital lending strategy. In fact, this type of digital + people hybrid approach to banking was born directly out of consumer demand.

It’s no secret that today’s consumers are more digital than ever. From their smartphones, tablets, and laptops they purchase everything online from luxury electric cars to their monthly supply of paper towels. So why shouldn’t they do their banking there as well?

Believe it or not, but the earliest digital banking experiences date back to the late 90’s. By the time the Great Recession rolled around in 2008, Alt Lenders and megabanks were already beginning to introduce the modern app experiences that we’re familiar with today. This head start is largely responsible for shifting consumers’ expectations to a place where they now believe their financial lives can primarily live online, as well.

What this means is consumers expect, and demand, the type of real-time, instantaneous buying experience from their local bank as they get from their favorite online retailer. And given the technology available today, there’s really no reason they shouldn’t.

What Is Real-Time Lending?

As our relationship banks begin to wrestle with this reality, they often find themselves at a crossroads. More conservative than their Alt Lender or megabank counterparts, relationship banks can’t simply pour billions into head-to-toe digital transformation. They need to find an entry point and they need to start where it can make the most impact for their bank.

Business lending is where the leaders in this space are headed and for good reason. The same consumers who want to do their banking on their smartphones are also the people running America’s more than 30 million small businesses—and they want convenience at work as well as in their personal lives.

From our in-depth look at real-time lending:

Real-time lending refers to the automated credit decisioning and funding of loans online - often instantaneously. The backbone of real-time lending is technology that allows banks to digitize their credit policies and underwriting processes while providing customers with a convenient online application experience.

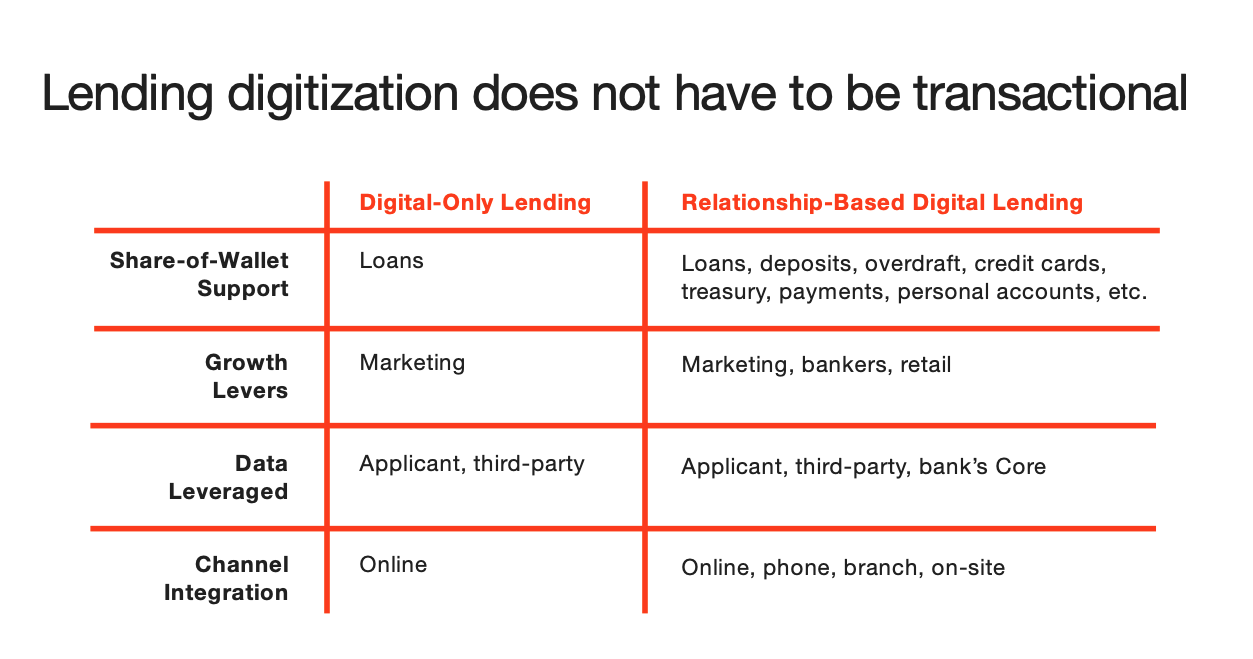

Real-time lending is just one part of relationship-based digital lending. Since the latter aims at offering customers the experience they prefer, where they prefer it, and when they prefer it, relationship-based digital lending offers an omni-channel approach.

For example, a customer may want to start an application online, continue on the phone, and then finalize it in the branch. For that to happen, bankers need to be able to pick up an application at any point in the process and provide a seamless experience. This can only be done if your bank has real-time lending capabilities.

Why Digital-Only Lending Experiences Fail

While many industries have looked at the technological revolution as a way to get more lean and efficient through automation, community and regional banks can’t afford to go that route.

Why?

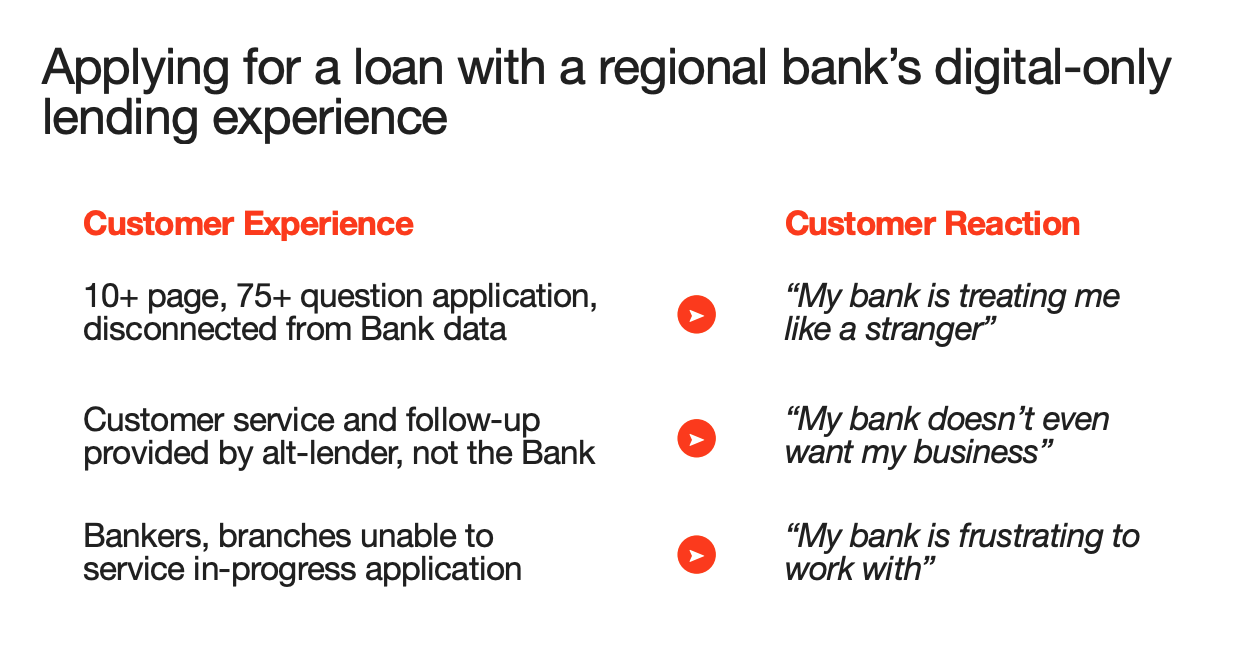

Because the digital-only lending experience completely discounts the human interaction, and human interactions are the cornerstone of the relationships that made these banks viable in the first place. And this is more than just a theory. We test drove a digital-only lending experience ourselves while developing Numerated’s relationship-based digital lending platform and discovered three areas in which these strategies fall short:

- They treat customers like strangers

- They provide a cold, indifferent experience—as if the customer’s business isn’t wanted

- They are difficult to work with and therefore hard to borrow from

Dan takes a deeper dive into this specific topic in our webinar, that you can watch on demand, here.

Why Outsourcing the Customer Experience Doesn’t Work

As we just mentioned, relationship banks are at a significant disadvantage when it comes to the resources they can spare, and the amount of risk they can take on, when considering digital transformation. Knowing where investments must be made, and where they can be temporarily delayed, is critical to finding the right balance between relationship and digital banking and, therefore, success.

Increasingly, bank leaders are telling us that customer service is just one area where corners cannot be cut. A common mistake made by community and regional banks occurs when customer service is outsourced to a third-party—typically an alt lender that the institution has struck some sort of referral partnership with.

There are many reasons why these outsourcing strategies fail, but as we’ve discussed in an in-depth article on the topic, some are more common than others. The five most common reasons these outsourcing strategies fail are because:

They offload the differentiating customer experience to a third-party organization

They don’t help bankers or branches provide better customer service or grow their relationships with customers

They take away a valuable “sandbox” for banks who are approaching digital transformation in piecemeal

They move the accountability for a poor customer experience outside of the bank, while still tying that poor experience to said bank

They represent a model that simply wasn’t designed for banks, and therefore they don’t satisfy the financial institution’s needs

Strategies For Banks In The Digital Era

Banking in the 21st century requires grappling with new realities. Community and regional banks are no longer competing amongst themselves. Rather, in the digital era they’re also competing with Alt Lenders, megabanks, and tech companies looking to disrupt yet another legacy industry.

Community and regional banks are also grappling with customers whose expectations have radically shifted during a turbulent decade. Customers, including small business owners, now expect and demand the convenience of digital but don’t want to sacrifice the service they’ve come to expect from their financial institutions.

Most community and regional banks aren’t currently equipped to face these realities, but know they must. Here, we take a look at what bank leaders should consider as they plot the next steps forward for their financial institutions.

Understanding and Evaluating Available Strategies

First and foremost, it’s important to remember that many of these community and regional banks are playing catch up when it comes to digital transformation. While this means that they need to operate with a sense of urgency if they want to remain competitive, it also means that they can learn from those who have gone before them.

This is especially important when we’re talking about the digital business lending segment which represents the most important growth opportunity for community and regional banks today.

As we’ve noted in a previous blog on evaluating digital lending strategies, banking institutions often look to “check the box” when it comes to digital lending. And, as Charles Wendel of Financial Institutions Consulting notes, this can inadvertently lead to an evaluation framework based on the path of least resistance.

This sort of thinking, of course, rarely leads to the best outcomes. When evaluating strategies, therefore, it’s important that banking executives ask themselves the types of questions that will help them take into account their current technology stack as well as their process and people flows.

Questions that fall under this category might include:

- Can you identify the lendable businesses in your markets?

- Do your business and retail bankers receive qualified lists of prospects?

- Do you want a customer experience that is consistent across channels?

Regardless of whether you download our list of 10 prescriptive questions here, or work on developing your own, it’s important that bank executives take these types of issues into consideration whether they’re building, buying, or partnering on digital lending.

Real-Time Lending Is A Winning Strategy For Regional And Community Banks

Leaders in the banking industry, like American Banker’s Paul Davis, have been sounding the alarm for community and regional banks for quite some time now, and their message is clear: You’re at risk of losing your business lending segment to Alt Lenders and megabanks.

But, as we’ve said a thousand times before, it’s not too late. We’re working with community and regional banks every day to address this specific strategic imperative and know there’s still time to win this David and Goliath battle.

In fact, there are relationship banks today—like Eastern Bank in Boston, MA—that are out-competing national digital lenders by finding the right balance between real-time lending and relationship banking.

While you can read an in-depth analysis of why these strategies are successful, here, it’s important to point out that real-time lending allows smaller institutions to provide an industry-leading digital experience, without eliminating the person-to-person relationships that made them successful to begin with.

Conclusion

Community and regional banks—that have historically made up the backbone of the American Banking Industry—are dwindling in numbers and facing existential challenges today. With Alt Lenders and megabanks flexing their technical advantages in the years following the Great Recession, these banks that have competed on relationships for years must now find new ways to win business in a digital era where consumer expectations have radically shifted.

If these banks are to find success, they’ll need to balance new investments with the relationship-banking tactics that have made them successful in the first place. Given their limited resources, and inability to take on big risks, these banks will need to be strategic in how they overcome new obstacles.

It’s our belief that the best way to accomplish this is through a relationship-based digital lending strategy, because it uses technology to enable and empower bankers and branches, rather than replace them.

To learn more about why relationship-based digital lending is the way forward, and why digital-only strategies fail, watch our on-demand webinar with Founder and CEO Dan O'Malley.